What Happened to Mortgage Refinancing?

Mortgage refinancing has been on a positive trend over the years prior to the covid-19 pandemic. According to Freddie Mac, the year 2018 had a refinance quota of 76.4% and 52.3% just before the pandemic.

But the pandemic has seen a dip in the refinancing of mortgages. The year 2020 recorded 35.7% and 2021 a 41.9%.

A more in-depth look at 2021 indicates that the American mortgage industry records just 19% of refinanced pre-pandemic mortgages in July. In contrast, over 47% have not given a thought to the concept of refinancing.

Therefore, according to the research, 74% of homeowners have not refinanced.

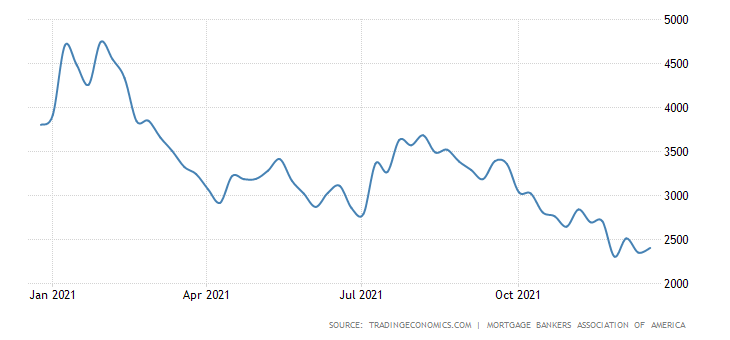

The USA MBA Mortgage Refinance Inde

Possible Reasons For The Dip In Refinancing

Let’s see a few possible factors that facilitate the dip in refinancing.

Increase in the Mortgage Rate

When mortgage rates slip, it tends to create a surge in refinancing. Here is a case study for the first week of December 2021.

According to reports from the mortgage bankers association, the mortgage rate fell on the first week of December, and mortgage application increased by 2%, leading to an increase in refinancing by 9%.

The mortgage bank chief forecaster Joel Kan stated that a drop in mortgage rate massively increased government refinances.

Therefore the relationship between both aspects is not linear; an increase in one tends to dip the other.

Change in Location (Especially during the pandemic)

Refinancing is ideal for borrowers who plan to keep the new mortgage for years. But in a case where a high number of people change geographic locations, it tends to decrease refinancing demand.

Other reasons include;

- High closing costs and fees

- Poor credit score etc.

Refinancing and The Non-QM Sector

After careful study of the refinancing index through the year, compared with the previous year, experts project the Non-QM market to grow substantially in 2022.

Data from the mortgage bankers association projects a 9% increase in purchase mortgage origination in 2022. This will rise to about $1.73 trillion; a record never achieved in the industry.

When there is a surge in purchase mortgage origination, it takes a down toll on refinancing. Little wonder the Mortgage Banker’s Association predicts a dip in refinance originations from $2.26 trillion to $860 billion. That’s a projected decrease of 62%.

Although it all looks gloomy when looking into refinancing a mortgage for the year 2022, It could also be a great year for the Non-QM sector.

Lesser refinancing activities push up the outright purchase of mortgages, which is good news for the Non-QM market. As a result, purchases will grow, and mortgage applications will surge.

How Does This Influence Non-QM?

Increase in Mortgage Purchase Action

When purchase action increases, it shows a high demand by mortgage borrowers. But, unfortunately, many tend to fall short and fail to qualify for the traditional mortgage out of the increasing stream of borrowers.

They turn over to Non-QM as an alternative. So it is expected that lenders in the Non-QM market will have a harvest of borrowers on the line.

Boosting the Fix and Flip Due to House Supply Shortage

Fix and Flip thrives in situations of house supply shortage. Statistics show that the U.S is short of about 4 -5 million homes. Fix and Flip encourages borrowers to renovate an existing home as it would become more appealing when put back into the market.

This will increase Non-QM chances to deal with Fix and Flip borrowers.

Other Influencers that can Boost Non-QM Growth

The flexibility and the lesser strict regulations of Non-QM are huge boosters. Due to the situation(Post covid era) around the globe, many borrowers are without jobs while others are self-employed. They will definitely turn over to Non-QM since it makes life easier for them.

Moving forward into 2022, the Non-QM can hope for substantial growth, and it is a message to lenders that they take advantage of the forthcoming opportunity.